Inflation + Recession = Stagflation

Opinion: New Normal Series

"If the American people ever allow private banks to control the issue of currency, first by inflation, then by deflation, the banks and corporations that will grow up around them will deprive the people of all property until their children will wake up homeless on the continent their fathers conquered." Thomas Jefferson

Wherever you are in the world and provided your name isn't Musk or Bezos (or another of that class), you will have noticed that stuff is costing rather more than it did a year ago. By that, I don't mean 5% or 6% more; I mean 30%-100%. And this stuff includes categories of goods and services that we cannot do without – fuel and food chief among them. Governments and central banks who primary role, lest we forget, is to keep us safe and fiscally viable are presiding over economies that are fubar. In essence, the most fundamental tasks that both institutions are charged with have proved to be beyond them.

By way of deflecting blame, individual regimes point to the fact that nearly all nations are encountering similar difficulties, as if this somehow lets them off the hook but even if all nations were equally afflicted, the authorities would still be culpable. As is becoming increasingly clear, nothing our lords and masters accomplish is by incompetence alone. Clearly, there are reasons for our current economic woes; they are just not the reasons that we are being fed and they are long way from unavoidable. There is, instead, method in the regimes' madness.

I shall concentrate on the US (although not exclusively), as any financial meltdown there inevitably ripples outwards by virtue of the delights of globalization, as the Global Financial Crisis (GFC) of 2008 ably demonstrated. In fact, 2008 is as good a starting place as any. Predatory lending, fraud and excessive risk taking by banks and other financial institutions resulted in huge losses but, naturally, all the big players – the ones who had caused the crash in the first place – were bailed out by the Federal Reserve bank. The Fed is a central bank (and most countries have got them), privately owned and the only current issuer of currency and setter of interest rates in America.

The GFC sparked the Great Depression and the European debt crisis, Iceland and Greece to the fore. In fact, although the focus is often on Greece and their national indebtedness, it is often forgotten that all three of Iceland's major banks failed which, pro rata, was the largest ever economic collapse by any country.(1) However, it was in America that truly epic losses and bailouts were most prevalent and the Fed's monetary policy was a significant contributing factor. In the early days of the new century, the Federal Reserve sought to prevent an economic slowdown by artificially keeping interest rates low, fearing a recession as a result of yet another piece of mismanagement resulting in the dot.com bubble imploding in the late nineties. The federal funds rate was cut from 6.5% to 1%, partly by virtue of deliberate design and partly of necessity as trade deficits resulted in the US borrowing money from abroad.

As previously noted, if the fiscally responsible cannot find a home for their savings within the financial system, because low interest rates are unattractive and savings accounts risk being outstripped by price inflation, where else might they invest instead, in the first instance? Traditionally, in bricks and mortar. However, it was apparent, as early as 2002, that a housing bubble was developing.

And so, 2003-2008 saw a prolonged housing boom; the desire to stave off an implosion saw the Fed pumping money into the economy, initially to the twelve Federal Reserve banks. These funds were then disbursed to other banks. And, as previously explained, the fractional reserve system ensured that multiples of the original sum were then loaned to businesses and consumers. Cheap mortgages abounded – there was so much available money that pretty much anyone could get a loan.

While the damage was eventually done by the packaging of sub-prime mortgages (meaning less than ideal) into financial instruments whose value was fraudulently inflated, the problem would not have existed if mortgages had continued to be paid, rather than defaulted on. But when the Fed raised the interest rate significantly between July 2004 and July 2006, the inevitable happened. Buyers who had not been properly vetted, some of whom had been given so-called ninja mortgages (no income, no job), found that their adjustable rate mortgage obligations rose exponentially. Payments could frequently not be made. Gradually, defaults accumulated and pressure built.

Having been responsible for causing the debacle, the Fed now stepped in to clear up its own mess. It swiftly became apparent that the solution with which it was most comfortable was to adopt the mantle of lender of last resort. Not content with having created multi billions of funny money in the previous five years or so, reducing the spending power of the dollar for ordinary Americans, their solution was to create and guarantee trillions more.

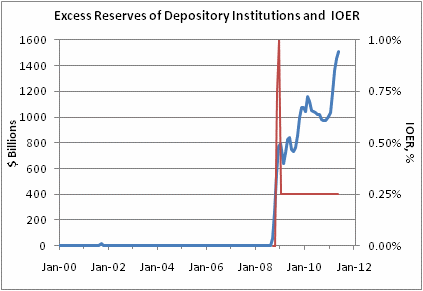

When the dust settled, the twelve largest banks in the country (all of whom had contributed hugely to the crisis and who had been within days of bankruptcy), now controlled 70% of all bank assets in the United States. The cost to the taxpayer, the actual total dollar value of the transfer of wealth from the ordinary American to the big banks, is difficult to calculate; largely due to the smoke and mirrors deployed by the Federal Reserve. Officially, spending and commitments totaled $16.8 trillion, not the $700 billion that the Treasury indicated it was.(2) It is also a matter of record that, from October 2008, the Fed started paying interest to banks on their mandatory reserves, reserves which were, at least partially, made up of the magic money that the Reserve was pumping into the banking system, in order to “stimulate the economy”.

Given the disastrous state of the economy and the fact that the markets were in a state of chaos, a good proportion of banks deemed it good business practice to keep hold of the money and earn interest from the Fed, rather than loaning the money and providing the allegedly desired stimulus. As late as 2012, banks were sitting on $1.5 trillion of reserves, instead of the $100 billion they were obliged to hold. Thus, economic recovery was stifled and the Fed let it happen.

There are many similarities between Fed policy in the first half of the noughties and Fed policy now, which I will come to shortly. However, in one crucial respect, conditions at the present time differ markedly and that is in the realm of inflation. In the period leading up to the GFC, inflation wasn't really an issue.

Figure 1 US inflation 1989-2009

Now, of course, it's the bane of our lives and, whilst the reasons for it are capable of being unraveled, its insidious presence has very little to do with Master Putin and rather more to do with Imposter Biden and the Fed.

Figure 2 US inflation now, according to the authorities

I should be clear about what I am taking the word 'inflation' to mean:

“The most classical description of inflation is “too much money chasing too few goods”; in other words the demand for goods and services exceeds the economy’s ability to supply those goods and services – and when products are scarce, prices rise. This comes under the remit of what is sometimes labelled as demand pull inflation.”(3)

So traditional 'inflation' is, in broad terms, the decline of purchasing power in a particular currency over time.(4) It's measured with reference to a basket of goods, known as the Consumer Price Index (CPI) or similar. This is supposed to provide a true measure of the effect on consumers but is, in fact, ripe for under-counting and inaccuracy. It depends what is actually in the basket of goods, what weighting is given to the various items, whether it's actually reflective of the costs that burden a typical consumer and whether it changes over time, for political reasons. Certainly, as one might expect, any changes that have been made to the CPI measure have had the effect of depressing reported inflation.

The British CPI has housing and utilities at 29% of the whole, transport at 13% and food at a mere 8%.(5) But, as prices rise on the absolute basics, what starts as a skewed formula becomes ever more irrelevant. I would venture that, for an increasing number of people, these three basic categories are consuming an ever greater percentage of earnings.

For instance, the CPI inflation rate that is being widely quoted (9.1% in the UK, 8.6% in the US and heading higher yet)(6) does not include fuel and energy prices in the US as these are deemed too volatile.(7) Seeing as how it's those very costs that are rising fastest, the usefulness of the headline rate is questionable, at best. The UK has a Producer Price Inflation Rate (PPI), which measures the rising costs that producers are enduring, and this is running at 15.7% (8) and, as we know, producers don't waste much time in passing costs onto the consumer. In the US, including fuel and food costs paints a rather different picture.

Figure 3 Alternative inflation calculation

Figure 4 Alternative inflation calculation including food and fuel

Take your pick; one is slightly less horrendous than the other, but both are well above official estimates and more in line with the pain that is actually being experienced. If one in six American households reported food insecurity twelve months ago,(9) what is it going to be like this year?

Inflation is also a transfer of wealth from people who rely on salaries to people who live off assets;(10) assets rise in value while, at least initially, wages don't. This is traditional inflation though, and traditional tools would usually work to reduce demand – notably, raising interest rates so that more people see the value of putting money on deposit rather than spending it. What we have currently is something else entirely and the measures that could be taken in order to remedy the situation have been foresworn.

What we have is stagflation, which is when demand stagnates but prices still keep going up:

“If the current momentum continues, the majority of necessities in the U.S. will not be affordable for most people by next year. We are looking at a fast-moving decline in production along with a swift explosion in prices. In other words, a stagflationary disaster.”(11)

This analysis is borne out by the facts; consumer debt (credit cards) is rising at the same time that savings are plummeting. In fact, savings are at their lowest ebb since 2008 and personal debt is at record levels.(12) At the same time, as we know, the things that we need the most are the things that are rising fastest in price:

“Consumers are in desperate straits. They are tapped out. Whatever savings they managed to accumulate during the pandemic when the government stuffed their pockets with stimulus money is gone. Now they’re maxing out their credit cards. And what are they buying? They’re only buying the necessities – food, energy, shelter. There is no money left for discretionary spending. This house of cards economy is on the verge of a collapse.”(13)

Somewhat unsurprisingly, a lack of funds for any service or activity that is not of fundamental importance leads to overall economic slowdown. Governments will obfuscate and deceive for as long as they possibly can – anything to avoid using the r word (recession), but the lesson of history is that recessions are upon us well before there is any acknowledgement of same and today is no different.

Figure 5 Real US GDP as against claimed GDP

So, how did we end up in such a position? A state of affairs where economies are tanking, but inflation is still raging higher? It turns out that it's not particularly difficult to divine; nor would it have been particularly difficult to avert. It takes an effort to screw things up this badly and Western regimes have been busting a gut in an effort to bankrupt us.

From 1980-2007, the US managed to sustain what is referred to as a 'Goldilocks economy', with moderate economic growth and low inflation. Interest rates came down in concert with inflation.(14) This is not to say that trouble wasn't brewing, as noted previously. Economic performance in the early 2000's, where bubbles were once again allowed to grow unsustainably large, was built on shaky foundations, a fact that became all too clear in 2008.

In the aftermath of the meltdown, the Fed - both the architect of the collapse and the lender of last resort that cleared up its own mess (at taxpayer's expense, naturally) – immediately started sowing the seeds of the next one. Interest rates were lowered to what were effectively negative rates and the system was flooded with 'funny money', created by the Reserve via a few strokes on a keyboard. They guaranteed the banks' debt and purchased their stock and, in the process, started accruing assets themselves. And they haven't stopped since.

Figure 6 US Fed Reserve balance sheet

This process, previously regarded as unconventional and a short term tactic that could be used when interest rates were very low, is known as Quantitative Easing (or QE):

“Quantitative easing (QE) is a form of unconventional monetary policy in which a central bank purchases longer-term securities from the open market in order to increase the money supply and encourage lending and investment. Buying these securities adds new money to the economy, and also serves to lower interest rates...”(15)

It's different from creating new money in response to legislation passed in the Senate because, with QE, the money goes to the banks and the assets that the Fed purchases go on its balance sheet. The money went to commercial banks, in exchange for assets, allegedly in order to stimulate the economy again. If interest rates are rock bottom, the consumers' incentive to save is diminished. In these circumstances, citizens with cash reserves hoard their money in the expectation that whatever it was that they wanted to buy would be cheaper tomorrow. Asset prices then fall and a recession begins. More money in the system , while inflationary, is an emergency measure that could force an economy out of recession. Interest rates are then raised and resume their role as the primary tool in the regulation of an economy.

This hasn't happened, largely because of the other action the Fed took. In 2008, for the first time ever, the Federal Reserve started paying interest to commercial banks on any excess reserves that those banks parked with the Fed themselves. So, the Fed bought these banks' assets, paid them with money that the Fed themselves had created out of thin air, and the banks then lodged that money back with the Fed as extra reserves, over and above the reserves that they are obligated to have. This had an immediate effect, but not on the economy.

Figure 7 US commercial banks excess reserves

Figure 8 US commercial banks excess reserves

Indeed, at the time of the GFC, banks had around $2 billion sitting with the Fed. Now, it's more than $3.6 trillion.(16) In an uncertain market, banks had found a way to still earn interest on the money that they were holding with zero risk. Compounding the problem, the Dodd-Frank Wall Street Reform Act was passed in 2010; this more closely regulated market activity and acted as a brake on lending.(17) Consequently, while the Fed kept on printing money, very little of it was finding its way into the actual economy.

Figure 9 US money creation

The green line is the money being lent out by banks. The red line is the money being created by the Fed and given to the banks in exchange for assets. And, of course, if the money isn't making it into the economy, there is no stimulation going on. Adding to the doom loop is the fact that, by buying up interest bearing assets such as bonds, the Fed is artificially depressing interest rates because the law of supply and demand works here also. If bonds are in demand anyway, there is no need for them to be paying out vast sums in interest; that is only necessary when buyers are in short supply.

The Americans weren't the only ones at it. The European Central Bank is also a prime culprit, as is the Bank of England and others. Worldwide, central banks have created over $11 trillion dollars of new money.(18)

Figure 10 QE in Europe

There is no conceivable way that these central bankers didn't know what they were doing. For them, it's banking 101. If the money isn't reaching the economy and interest rates are being depressed by demand for bonds, raising the official interest rate is a non starter. The QE cycle must continue. The problems (in the US, at least) is that firstly, the cycle isn't sustainable and, secondly, what happens if and when the excess trillions of dollars do somehow make it out into the economy? Not all of it was being placed with the Fed as excess reserves. Some of the money (around 20%) was actually being loaned out.

But very little of it was going to the man on the street; most of it was going to publicly traded corporations. And what were they doing with it? Well, they weren't investing much in infrastructure or building long term resilience. They were buying their own stock back on the markets and paying shareholders their dividends with it. And why would they do that? They still are. In fact, records are being broken. So far this year, $319 billion of share buy-backs have been announced, up on $267 billion at this time last year.(19) And why would they do that? Because, in doing so, they keep the price of their stock artificially high, they reward themselves and they reward their shareholders....in the short term, that is:

“A Roosevelt Institute study found that whereas firms once borrowed to invest and improve their long-term performance, they now borrow to enrich their investors in the short-run.”(20)

The modern day CEO has a rather unusual salary structure. There is usually a small wage which is dwarfed by stock allocations. The idea, which has its origins in academic writings in the 1970s, is that the CEO is incentivised to grow the company because they will benefit when, at some as yet undesignated moment, they sell their stock. What is actually happening is that companies are borrowing money so that they may buy specific stock; the CEO's and favored investors, in particular.(21) The entire concept has, therefore, been corrupted. Money that could be utilized in growing the company is instead used to enrich certain parties in the short term, to the detriment of the company in the long term. Not only that, but buying when the price is high (and, trust me, prices have been high for years) also increases the fragility of the company.

Figure 11 US companies buying back stock at high cost to themselves

“Taking on debt to finance buybacks, however, is bad management, given that no revenue-generating investments are made that can allow the company to pay off the debt. Stock buybacks made as open-market repurchases make no contribution to the productive capabilities of the firm.”(22)

Historically, a company might buy-back its own stock if it were planning to go private – there have been some instances of that. But borrowing money to buy stock, simply in order that they might drive up the share price, rather than trust that share value will increase by virtue of company performance is simply building a house of cards. Price to earnings ratios used to be in the region of 10. Some stocks in the US are now at 75-80. The entire stock-market is buoyed up by buy-backs, which is in turn reliant upon commercial banks' loans, which relies on the Fed buying the banks' assets via QE. It's not difficult to see what might happen if the spigot is turned off. Yes, the banks have excess reserves, but they may not be too keen to throw good money after bad.

So far then, we have the central bankers creating money, ostensibly in a bid to stimulate economic activity, which they immediately undermine by virtue of interest paying excess reserves accounts. They have bloated their own balance sheet (that's our balance sheet, by the way) by acquiring risky assets from the banks – including vast tranches of mortgage backed securities (MBS) that will plummet in value when yet another housing boom goes pop) – and giving them cash.

In the process, they have ensured that interest rates remain at rock bottom, thus leading to inevitable stock market speculation by private citizens and funds alike, because safer investment vehicles (such as bonds or savings accounts) do not offer an adequate return. And by deliberately depriving themselves of conventional monetary tools, they have made QE a permanent feature of the landscape; which is an unsustainable practice. Finally, commercial bank loans have barely impacted the economy, as they have served to simply sustain a stock-market bubble, and monies that might have been used to improve the supply side have been squandered on self serving buy-backs.

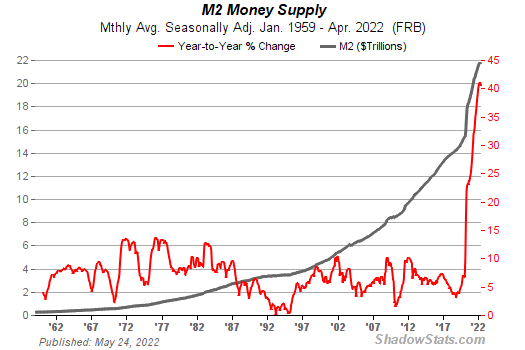

But there's more and, once again, it's kindergarten level knowledge for economists. Given the monetary landscape at the end of 2019, the fragile nature of the economy, one might have been able to speculate on what set of circumstances would be most damaging. I would submit that a production lock-down leading to the mothballing of factories and supply chain snafus, followed by a massive injection of cash into the economy at the point at which businesses started to reopen, with a side dish of a shortage of workers (leading to some additional inflation in the form of wages) would be one of the scenarios to avoid but, as we know, that's exactly what we got. The Fed may not have been expanding the M2 money supply prior to 2020, but the government did the job for them in the year of the 'pandemic'. Federal debt has tripled since 2008; it currently sits at around $30 trillion and these particular funds went straight into the economy.

Figure 12 US real money supply into economy

It was widely known that the stimulus checks were an overreaction and that a large chunk of the money would be spent on chasing nice-to-have items, rather than on essentials. Broadly speaking, it works like this:

“Imagine an economy with $100 and 100 bananas. If everyone were to take their money and buy all bananas, the average price per banana would be $1. Now imagine the government increased the money supply by 10% to $110, but this fictitious economy was only able to grow banana output by 5% to 105 bananas. Since the amount of money increased more than the number of bananas, the average price per banana now increased to roughly $1.05.”(23)

It was also widely known that 'vaccine' mandates would have a deleterious effect on the workforce. Lastly, one doesn't need to be a Nobel Prize winner to realize that supply chains would be severely compromised, nor that it wasn't Covid that shut everything down with no thought as to the consequences; it was the regimes.

Regime actions led directly to an initial round of traditional demand side inflation, but that has fizzled out now. What wasn't foreseen (but should have been, given the climate change rhetoric and the character of the US administration's leading figures) is that their policies and many instances of outright sabotage would comprehensively ruin the supply side, too. The key to all the destruction being visited upon that side of the equation is energy.

The fuel (energy) crisis is being driven by several factors and only one of them rhymes with hootin'. As the oil companies reminded Biden, when he recently chided them:

"While members of your administration have recently discussed the need for additional supplies to solve the energy crisis, your administration has restricted oil and natural gas development, canceled energy infrastructure projects, imposed regulatory uncertainty, and proposed new tax increases on American oil and gas producers competing globally."(24)

This is not a welcoming environment. Uncertainty limits investment. The oil companies know that the administration is coming for them; they have no reason to invest long term, because they can clearly see that long term doesn't exist. In the past, rising oil prices would have prompted them to ramp up supply, but increasing red tape and a trend that chokes off access to development capital, has rendered them largely impotent.

The second factor is indeed the cost of crude oil, but it's a little more complicated than the talking heads would have you believe. Much is made of America's alleged energy independence, recently squandered by Biden, but this is misleading. The US was a net exporter under Trump, yes; but that doesn't mean that all the oil and gas produced by American oil companies was consumed by the American people, with the excess exported. Not all oil is the same and not all refineries can refine every type of oil.

Foreign oil (frequently heavy crude oil) arrives at US ports and is refined. However:

“Since the U.S. energy renaissance has accelerated, however, most of the 4.8 mb/d of new U.S. oil production the past six years has been light oil. With U.S. refining capacity geared toward a diverse crude oil slate, a key implication for U.S. petroleum trade is that it would be uneconomic to run refineries solely on domestic light crude oil. Consequently, the United States:

Must import crude oil of different qualities to optimize production, given its mix of refining capacity; and,

Has more light crude oil than it can handle domestically, while this same quality of oil is in high demand in Asia Pacific and other regions that mainly have simple refineries (without conversion capacity).”(25)

It's the mix that is important. And there are growing problems with refining capacities in the US (and elsewhere; UK refining capacity has dropped 30% since 2011)(26). Since 2019, overall US refining capability has declined by 5.4% (27), which doesn't seem much, but it does mean that the refineries are running at 94% capacity and all the product is going out the door – reserves are at historically low levels.(28) The gas and oil that US companies produce is finally able to be exported; they were banned from doing so until recently and, ironically, by selling their product for the best price on the world market, they are contributing to price rises back home. Exports of gasoline, diesel and jet fuel are up to 32%, year on year.(29)

Sanctions on Russia obviously haven't helped. Because of the fact that the US still relies on foreign producers for its heavy crude oil, it is vulnerable to the same stressors as other countries, although not to the degree of Western Europe. Nonetheless, attempts to punish Russia have rebounded spectacularly on the US if, indeed, that has ever been the true intention. The Russian currency is flying high (higher than it was before sanctions) and many EU members have succumbed to Russian demands that they abandon petrodollars and pay in rubles, thus weakening the dollar.

Figure 13 Brent crude oil price per barrel

But, as can be seen, prices were already trending much higher before the war in Ukraine. There is more going on and the likes of Warren Buffet's Berkshire Hathaway, Vanguard, BlackRock and State Street (all investment funds) are in the thick of it. The CEO of Pilot and Flying J, a company responsible for the transportation of 20% of America's diesel supply stated (when testifying) that Union Pacific Railways had demanded that his company cut 26% of their shipments or the railway would embargo them. They later raised their stipulation to 50%.(30) No explanation was offered. Warren Buffet owns a third of Pilot and Flying J's stock. The top three investors in Union Pacific are the other aforementioned funds.

There is further meddling in Exxon's boardroom. Activist investors at a fund called Engine Number 1 managed to obtain four seats on the board of directors, despite owning only 0.02% of company stock. They succeeded because they they were backed by the three largest shareholders; BlackRock, Vanguard and State Street again. These investors are now trying to impose their own global warming policies on an oil company.(31) It's that sort of development that makes what's happening in the here and now seem more likely to be permanent than temporary. When the president says this:

“My mother had an expression: out of everything lousy, something good will happen. We have a chance to make a fundamental turn toward renewable energy, electric vehicles, and across the board”.(32)

it would be wise to conclude that mitigations and U turns are not on the agenda. To recap; the US is now more vulnerable to global energy prices, a side effect of its own exploitation of its fossil fuel reserves. The administration has left no doubt as to its intentions; it will tie oil companies up in red tape and create a regulatory atmosphere that discourages investment. It openly talks about eliminating fossil fuels. All of this has an effect on energy prices. Meanwhile, the private sector part of the cabal is ensuring that less fuel gets to the pump and because energy is needed to make and transport the vast majority of products, costs across the board have risen and will continue to do so.

“The BBB plan disrupted the supply side, then triggered a reopening of the demand side while the supply remained scarce. Simultaneous to the reopening, all former energy development processes were no longer supported by investment or policy. In the aftermath, the energy sector was fractured and, combined with higher costs for the production of all goods, that's what is continuing this upward inflation spiral.”(33)

That's without the separate pressure being applied to food production in the US with an exponential rise in fires at food processing plants and an unprecedented culling of livestock; 34 fires (against a yearly average of 2), two light aircraft crashes and over 35.5 million ducks, chickens and turkeys destroyed.(34)

The Federal Reserve (and, by implication, the US state) has worked long and hard on this scheme and they have managed to approach the denouement virtually undetected, by which I mean undetected as to intent. However, the 'mistakes' they've made are egregious. An example; why provide an interest bearing safe haven for excess reserves if the intention is to get those funds into the economy? Even if we allow a little latitude – perhaps they misjudged the commercial banks' wariness in the immediate aftermath of the GFC – why keep paying interest once it became apparent that the plan wasn't working?

Why did the Fed deprive themselves of their most effective weapon by leaving interest rates in the basement, thus wedding themselves to QE? Why can they not recognise that a recession is looming in the midst of an inflationary inferno and that a traditional response to inflation alone (finally raising interest rates, which they have now done) will only exacerbate problems by making debt more expensive for people who are already drowning in it in attempting to survive and that the problem lies with the supply side? Their own figures confirm it -

“US Manufacturing PMI fell dramatically to 52.4 in June 2022 from 57 in May. This drop is well below the market and economic expectations of 56, and now points to the slowest growth and steepest drop in factory activity in almost two years.

Production and new sales declined for the first time since the depths of the pandemic in mid-2020 driven by weak consumer demand. Inflation and a drop in wholesale and retail purchases have lowered purchase orders.”(35)

Might raising interest rates also prompt the commercial banks to put some of those excess reserves to work by loaning them out, thus increasing the money supply and creating more inflationary pressure? And lastly, why can't they see that announcing that they are going to reverse QE and start taking money out of the economy instead – right at the onset of a recession – will make matters worse?(36) They tried weaning the banks and the market off QE in 2018 and it didn't go well; the S&P index lost 6% and, after ten months, the Fed gave up and restarted QE.(37) What is being proposed now is four times more drastic – something that's never been attempted before.

The answer to all those questions is that they can see it. They made it happen; of course they can see what they've done. None of the measures they have inflicted on us over the past couple of decades have been off-the-cuff decisions. They (and others like them) are not high school economics students. They know that they've created stagflation and they know that if they pretend it's just inflation instead, they can get away with more counterproductive policies without us noticing. They are devastating the supply side for the basics; the inevitable result of that will be a jolting economic slowdown in all nice-to-have sectors and rising prices for all essentials, which is exactly what's happening. And, given that their actions are driven by a combination of ideology, arrogance and callousness, there is no likelihood of them reversing course unless they're forced to.

Conclusion

Regimes (and their bankers) are getting far too easy a ride. The vast majority of analysts, if they disagree with policy at all, tend to say that the Fed or the ECB are mistaken in their actions. They give no thought to the possibility that the policies are, in fact, having the desired effect. And these central bankers are not in the process of fouling up some obscure financial sector or small, unloved segment of society. They are deliberately torpedoing the current and future prospects of an overwhelming majority of citizens in order to 'reset' entire continents in a configuration that benefits the few at the expense of the many.

There are a good many moving parts within the overall scheme, as I am seeking to demonstrate in this series of essays; ongoing 'pandemics', programmable digital currencies, repression, censorship and increased surveillance being some of the more notable. The attempt to impoverish us, the people, is an intrinsic part of that plan, as it is the best way to ensure that we are helpless and dependent and, necessarily, desperately grateful for whatever coercive, sub optimal solutions they offer us.

If you recall, the WEF (coiners of the Build Back Better slogan which is parroted by every Western leader) has told us that we will own nothing and be happy about it. It's safe to say that the first part of that declaration is far more important (to them) than the second. The only reason they would pay the slightest heed to our happiness would be in order that they might better calculate our compliance threshold.

Why did the central bankers keep interest rates so low, even when economies recovered after the GFC? Why did they use QE instead? The much vaunted recovery from the financial crisis seems to be mostly illusory:

“Production of fiat money is not the same as real production within the economy… Trillions of dollars in public works programs might create more jobs, but it will also inflate prices as the dollar goes into decline. So, unless wages are adjusted constantly according to price increases, people will have jobs, but still won’t be able to afford a comfortable standard of living. This leads to stagflation, in which prices continue to rise while wages and consumption stagnate.”(38)

Stagflation is designed – for the regimes, it's another (albeit outsized) brick in the wall of our subjugation. They genuinely do not care about the harm that they are doing; we are just the inevitable collateral damage that ensues when they assert their natural right to dominance. However, what we are currently enduring – catastrophic though it certainly is for some – is designed to be a mere staging post. These conditions, if they are allowed to persist, will inevitably lead to a humongous financial implosion which will, in turn, lead to a depression that will dwarf the fallout from the GFC. It is to that happy scenario that I turn next.

Citations

(1) https://en.wikipedia.org/wiki/Financial_crisis_of_2007%E2%80%932008

(2) https://www.forbes.com/sites/mikecollins/2015/07/14/the-big-bank-bailout/?sh=30a2719d2d83

(3) https://www.politics.co.uk/reference/inflation/

(4) https://www.investopedia.com/terms/i/inflation.asp

(5) https://www.economicshelp.org/blog/54/inflation/how-is-inflation-calculated/

(6) https://www.irishtimes.com/business/economy/2022/06/22/uk-inflation-hits-91-as-food-prices-soar/

(7) https://www.forbes.com/advisor/investing/how-to-calculate-inflation/

(8) https://www.ons.gov.uk/economy/inflationandpriceindices/bulletins/producerpriceinflation/may2022

(9) https://cronkitenews.azpbs.org/2021/08/31/food-insecurity/

(10) https://hivebusiness.co.uk/insights/why-youre-not-supposed-to-know-the-real-inflation-rate

(11) https://www.zerohedge.com/political/fed-has-triggered-stagflationary-disaster-will-hit-hard-year

(12) https://www.zerohedge.com/economics/we-are-hurtling-toward-stagflation

(13) Ditto

(14) https://www.zerohedge.com/news/2022-03-12/structural-stagflation-enemy-goldilocks-economy

(15) https://www.investopedia.com/terms/q/quantitative-easing.asp

(16) https://www.dailywire.com/news/bank-of-england-joins-the-fed-in-warning-of-more-pronounced-inflation

(17) https://en.wikipedia.org/wiki/Dodd%E2%80%93Frank_Wall_Street_Reform_and_Consumer_Protection_Act

(18) https://www.ecb.europa.eu/mopo/implement/app/html/index.en.html

(21) https://medium.com/rantt/stock-buybacks-are-a-parasite-on-the-us-economy-d0369364c37e

(22) https://hbr.org/2020/01/why-stock-buybacks-are-dangerous-for-the-economy

(23) https://www.investopedia.com/ask/answers/042015/how-does-money-supply-affect-inflation.asp

(24) https://reason.com/2022/06/17/blame-high-gas-prices-red-tape/

(25) https://www.api.org/news-policy-and-issues/blog/2018/06/14/why-the-us-must-import-and-export-oil

(26) https://www.statista.com/statistics/332158/refinery-capacities-in-the-united-kingdom-uk/

(28) Ditto

(29) https://www.wsj.com/articles/high-u-s-fuel-exports-are-contributing-to-5-a-gallon-gas-11655371801

(30)

(32) https://www.independentsentinel.com/biden-suggests-hes-pleased-with-the-high-price-of-gasoline/

Figure 1

Figure 2

Figure 3 http://www.shadowstats.com/alternate_data/inflation-charts

Figure 4

Figure 5 http://www.shadowstats.com/alternate_data/gross-domestic-product-charts

Figure 7 https://seekingalpha.com/article/274561-so-where-did-all-that-qe-money-actually-go

Figure 8 https://fred.stlouisfed.org/series/TOTRESNS

Figure 9 https://prudentfinancial.com/investment/2021-05-04-is-the-fed-really-juicing-the-stock-market/

Figure 10 https://www.ecb.europa.eu/mopo/implement/app/html/index.en.html

Figure 11 https://hbr.org/2020/01/why-stock-buybacks-are-dangerous-for-the-economy

Figure 12 http://www.shadowstats.com/charts/monetary-base-money-supply

Figure 13 https://img.iex.nl/charts/issueCloseprice.ashx?sc=638&history=6&id=501435972&compare=0